№ 016 · Strategy · · 11 min

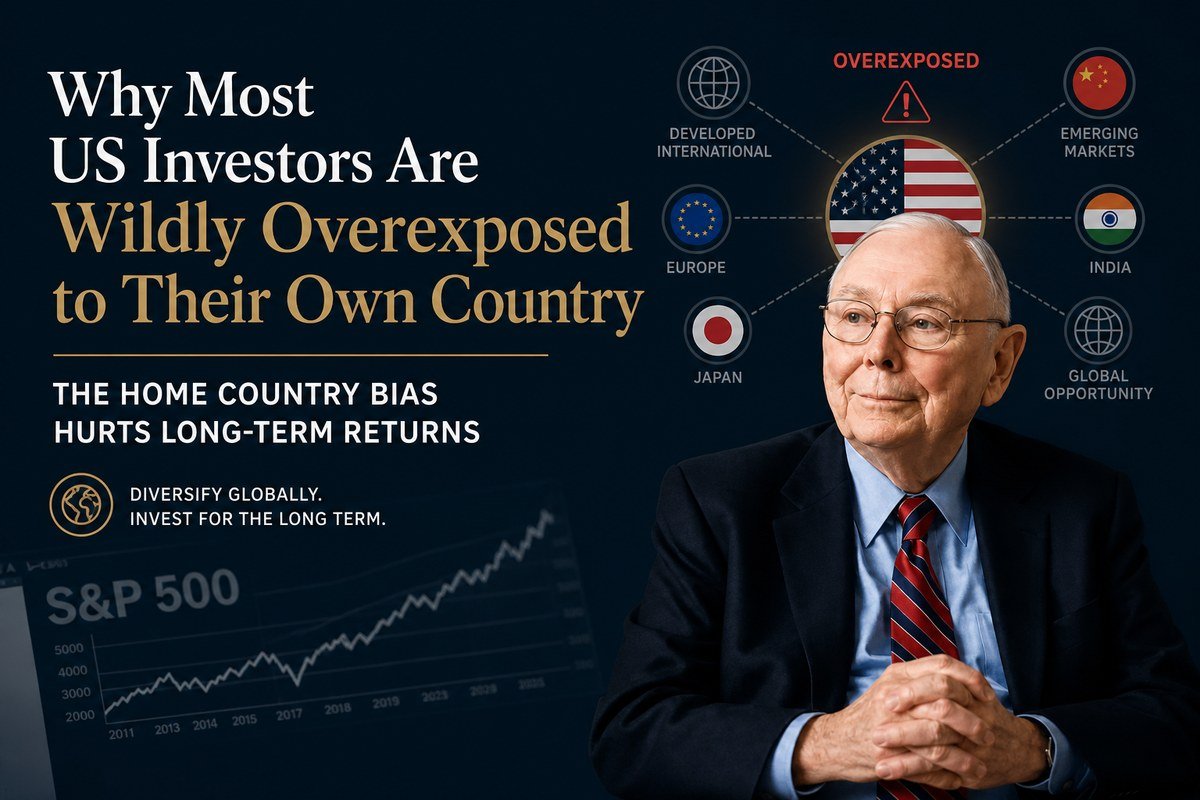

Why Most US Investors Are Wildly Overexposed to Their Own Country

US investors typically hold 55–65% of their equity portfolios in domestic stocks despite the US representing roughly 35% of global market capitalization. This structural overweight is a behavioral bias masquerading as a strategy.

There is a number that should make every US equity investor pause. The United States represents approximately 35% of global equity market capitalization. Yet survey after survey, and portfolio audit after portfolio audit, finds that US retail investors and many advisor-managed accounts hold somewhere between 55% and 65% of their equity exposure in domestic stocks. The gap between those two numbers is not a strategy. It is a bias, and it compounds quietly across decades.

This article is not an argument that international stocks are about to outperform, or that the US market is overvalued today. Those are separate questions. This is an argument about structure: that holding nearly twice your market-cap-neutral weight in a single country, for psychological rather than analytical reasons, is a form of portfolio risk that most investors never consciously chose and rarely reassess.

The Math vs. The Reality: What Market-Cap Weighting Actually Implies

Start with the neutral baseline. A portfolio weighted by global market capitalization, broadly following something like the MSCI ACWI, allocates roughly 35% to the United States and 65% to the rest of the world. That rest-of-world bucket includes developed markets in Europe, Japan, Australia, and Canada, as well as emerging markets across Asia, Latin America, and elsewhere. The specific percentage shifts over time as relative valuations move, but the rough proportions have been fairly stable: the US is large, but it is not the majority of investable equity wealth on earth.

A portfolio sitting at 60% US and 40% everywhere else is not a globally diversified portfolio. It is a US portfolio with an international sleeve. The distinction matters because the risk profile, currency exposure, sector composition, and cyclical behavior of those two constructions are genuinely different over long periods.

Market-cap weighting is not a perfect framework, but it is the most defensible neutral starting point. Any meaningful deviation from it is an active bet, whether the investor recognizes it as one or not.

For investors who use all-in-one global ETFs, it is worth noting that even those products often embed some degree of home bias for their domicile. Vanguard’s VEQT, for example, currently carries roughly 45% US weight. That is already above pure global market-cap weight, and it still represents significantly more international diversification than most self-directed US investor portfolios. The point is not that VEQT is flawed. The point is that even a fund designed for broad global exposure lands above the neutral market-cap weight when it incorporates a deliberate home-country tilt for Canadian investors. US-domiciled investors constructing their own portfolios rarely apply even this level of discipline.

How Overconfidence Scales from Stock Picking to Country Allocation

Behavioral finance has spent decades documenting how overconfidence distorts individual stock selection. The foundational work by researchers including Kahneman, Tversky, Odean, Malmendier, and Hirshleifer established that investors systematically overestimate their ability to identify winning securities, attribute successful outcomes to skill rather than luck or market conditions, and trade too frequently as a result. Research on self-attribution bias finds a strong positive relationship between market returns and subsequent trading turnover: when markets rise, investors conclude they were right, and they act on that conviction.

What receives less attention is how this same dynamic operates at the portfolio allocation level rather than the individual stock level. When an investor watches the S&P 500 outperform international indices for a decade, the psychological mechanism is identical to watching a stock they picked rise sharply. The instinct is to attribute the result to judgment: “I was right to favor the US.” The correct question, almost never asked, is whether the outcome reflected skill or a period of cyclical leadership that happens to have lasted longer than most.

Research on overconfidence among high-net-worth investors finds consistent evidence that success breeds conviction rather than humility, and that overconfident investors systematically underestimate risks they are not tracking closely. For a US investor whose international exposure has lagged for years, the risk of non-US equities feels vivid and recent, while the risk of US concentration feels abstract. That asymmetry in perceived risk is itself a bias, not a reasoned conclusion.

The Outperformance Trap: How a Decade of US Leadership Creates the Worst Allocations

The period from roughly 2015 through 2024 was a genuine era of US equity dominance. Technology sector concentration in the S&P 500, combined with dollar strength and the scalability economics of platform businesses, produced returns that dwarfed most developed international and emerging market indices over that window. That is simply true. The question is what investors should conclude from it.

The behavioral error is what researchers call self-attribution at the portfolio level: interpreting a cycle of outperformance as evidence of a permanent structural edge. US investors who leaned domestic during this period did well, and they drew the natural but potentially wrong conclusion: that their preference for US equities was analytically justified rather than fortunate timing. As a result, many portfolios that started 2015 at 55% US had drifted well above 65% US by 2024, not through deliberate rebalancing upward, but through simple neglect as US holdings grew faster than international ones.

This is precisely the worst moment to be most overweight. Asset allocation drift driven by performance means that investors accumulate the most exposure to an asset class precisely when its relative valuation is highest relative to alternatives. The mechanical result of ignoring rebalancing during a period of US leadership is that investors bought more US exposure implicitly at the top of a relative performance cycle.

Historical Cycles: When International Led, and Why That Matters

The phrase “US equities always win long-term” is recency bias treated as natural law. The historical record is considerably more complicated. During the 1970s, international developed markets materially outperformed the US as dollar weakness and commodity cycles favored other economies. Through much of the 1980s, Japan’s equity market produced extraordinary returns, and European equities were competitive with US indices. The decade from 2000 through 2009, the so-called “lost decade” for the S&P 500, saw emerging market equities deliver strong absolute returns even after accounting for volatility, with Brazil, China, and other developing economies compounding substantially while US investors in domestic index funds essentially broke even or lost ground in real terms.

Even the period from 2010 through 2015, which preceded the sharpest phase of US outperformance, saw meaningful parity between developed international and US returns in several years. The historical record does not support the conclusion that any single country’s equity market permanently leads over all long horizons. What it does support is that leadership cycles exist, they last long enough to feel permanent, and they reverse in ways that surprise investors who had drawn permanent conclusions from temporary conditions.

The investor who says “international has underperformed for a decade, so I am reducing my allocation” is doing the opposite of what sound portfolio construction requires. They are selling low on relative value and buying high on recent momentum.

What a Defensible Allocation Actually Looks Like

Given the neutral baseline of approximately 35% US in global market-cap weight, what is a rational range for a US investor who wants some tilt toward their home market? There are legitimate arguments for a modest overweight. US-based investors earn income, hold assets, and will spend in retirement in USD, which gives them a genuine currency hedge argument for owning more US equities than a purely global weight would suggest. US regulatory and legal infrastructure for corporate governance is well established. And the technology sector concentration in US indices does represent real economic value that a purely geographic framework might underweight.

These arguments support a modest home tilt, not a structural doubling of market-cap weight. A reasonable defensible floor for US equities in a globally diversified equity portfolio is around 40%. A ceiling of roughly 55% is supportable only with an explicit, written conviction thesis about why the investor expects continued relative US outperformance, combined with a rebalancing discipline that will reduce US weight if it drifts higher through performance. Allocations above 55% with no rebalancing plan are not a strategy. They are the accumulated residue of behavioral drift.

For investors currently sitting at 65% or more in US equities, the practical question is not whether to go cold turkey to 35% overnight. Currency adjustments, tax implications in taxable accounts, and transaction costs all matter. The actionable move is to set an explicit target range, stop adding to US equity overweights through new contributions, and redirect incremental investment toward international and emerging market exposure until the allocation converges toward the target band.

Rebalancing as the Structural Cure for Behavioral Drift

Academic finance literature has documented rebalancing as one of the few genuine sources of return improvement available to passive investors without requiring skill or prediction. The mechanism is simple: selling relative winners to buy relative laggards is a systematic way of harvesting mean-reversion tendencies across asset classes. Research consistently finds that annual or semi-annual rebalancing produces better risk-adjusted outcomes over long periods than portfolios left to drift, primarily by preventing the accumulation of extreme concentration in recent winners.

For the home bias problem specifically, a rebalancing rule anchored to an explicit target range does something even more valuable: it removes the psychological decision from the equation. An investor who has written down “I will maintain 40, 50% US equity weight and rebalance annually when any allocation drifts more than 5 percentage points from target” no longer has to make a judgment call about whether US or international equities will lead next year. They simply execute the rule. That mechanical discipline is the practical antidote to the overconfidence and self-attribution effects that create the problem in the first place.

A rebalancing policy converts what would otherwise be a series of emotionally influenced allocation decisions into a single, well-reasoned rule made at a moment of clarity. That is the structural advantage it provides.

The specific rebalancing frequency matters less than having a policy and following it. Annual rebalancing is simpler to implement and incurs lower transaction costs than quarterly reviews. For taxable accounts, rebalancing through new contributions rather than sales can reduce tax drag while still moving allocations toward targets over time. The point is the discipline, not the precise schedule.

The Practical Step Most Investors Skip

Most investors who are aware of home bias intellectually still fail to act on it because the correction requires doing something uncomfortable: buying assets that have underperformed. International developed and emerging markets have lagged the S&P 500 badly over the recent cycle. That lag is precisely the reason the opportunity for relative value is worth considering. It is not a prediction that international markets will outperform tomorrow. It is an acknowledgment that sustained underperformance is a condition that eventually ends, and that holding diversified global exposure means not needing to predict when.

The concrete action is straightforward. Calculate your current equity allocation by geography. Compare it to a market-cap-neutral baseline of approximately 35% US. Assess whether your deviation from that baseline reflects deliberate analytical conviction with a clear rebalancing plan, or whether it reflects passive drift accumulated during a favorable decade. If it is the latter, the portfolio you are holding today was not designed. It happened to you. And the correction is simply to take back control of it systematically, without drama, and without waiting for a signal that never comes.

Frequently Asked Questions

Q: Is there a specific US allocation percentage I should target?

A: A market-cap-neutral weight for the US is approximately 35% of global equities. A defensible range for US-based investors, accounting for currency and regulatory familiarity, is roughly 40, 50%. Anything above 55% requires an explicit rationale and a rebalancing policy to hold responsibly. These are not rules, but they are informed reference points.

Q: Won’t I miss out on US gains if I reduce my domestic exposure?

A: You will capture the portion proportional to your allocation. The implicit assumption behind “missing out” is that US outperformance is permanent rather than cyclical. That assumption is not supported by the historical record. A globally diversified portfolio participates meaningfully in US gains while also capturing growth when other regions lead.

Q: How do I add international exposure without overcomplicating my portfolio?

A: The simplest path is a single all-world ex-US fund combined with a separate US equity fund at your target weight. Alternatively, a globally diversified all-in-one equity ETF brings you closer to market-cap weights in a single holding, though even those products often carry some home tilt. The goal is deliberate simplicity, not complexity for its own sake.

Q: Does this analysis apply to investors outside the US?

A: Yes, with adaptation. Home bias is documented in virtually every investor population globally. Canadian investors historically overweight Canadian equities far above Canada’s roughly 3% global market-cap weight. UK investors overweight UK stocks. The behavioral mechanism is universal. The specific neutral weight and the arguments for modest home tilts vary by country, but the core principle, that deviation from market-cap weight requires a conscious rationale and a rebalancing discipline, applies everywhere.