№ 001 · Strategy · · 11 min

Buffett’s Real Edge Wasn’t Stock Picking, It Was Patience

Most investors focus on which stocks Buffett bought. The more instructive question is how long he held them, and what that holding period alone contributed to his returns.

Warren Buffett has been studied, quoted, and imitated for decades. The analysis almost always focuses on the same questions: How did he find Coca-Cola before the market fully appreciated it? What made him see the moat in See’s Candies? How did he recognize American Express was mispriced after the salad oil scandal? These are reasonable questions, but they are also the wrong ones if you are trying to extract a lesson that is actually usable.

The more important question is not what Buffett bought. It is how long he held it, and what that holding period alone contributed to the final number. When you run that analysis honestly, the conclusion is uncomfortable for anyone who thinks of investing as a skill game centered on selection: patience, more than insight, is the primary driver of Buffett’s compounding record.

The Myth of the Brilliant Stock Picker

Buffett is genuinely a skilled analyst. Nobody serious disputes that. But skill in identifying undervalued businesses is far more common than his record suggests it should be. Thousands of trained analysts read the same filings, apply the same discounted cash flow frameworks, and attend the same industry conferences. Very few of them come anywhere near Berkshire Hathaway’s long-run numbers. The differentiating variable is not primarily analytical horsepower. It is time horizon.

Berkshire first purchased Coca-Cola shares in 1988. As of the time of this writing, that position is still held, nearly four decades later. The cost basis on that original purchase is a small fraction of the current market value. The gain is not the result of buying at a cleverly timed low and selling at a cleverly timed high. It is the result of buying at a reasonable price and then doing almost nothing for an extraordinarily long time while the business compounded its own value.

The stock market is a device for transferring money from the impatient to the patient. That single Buffett observation contains more practical investing guidance than most books written about him.

American Express has been in the Berkshire portfolio since the 1960s, with additional purchases made across different periods. Wells Fargo (held for decades before its eventual reduction), Washington Post, GEICO before full acquisition: the pattern is consistent. The positions that generated the most wealth were not the ones where Buffett timed a clever exit. They were the ones he simply refused to sell.

What a 5-Year Flip Strategy Would Have Produced

Consider a thought experiment grounded in how compounding actually works. Suppose an investor had matched Buffett’s entry into Coca-Cola in 1988 but, rather than holding indefinitely, had sold after five years, taken the gain, paid capital gains tax on it, and then reinvested in the next best idea. Repeat that process every five years across the same universe of stocks Buffett owned.

The first problem is that the five-year return on any of these names, while solid, would not have been extraordinary. Coca-Cola returned strong but not spectacular numbers in any isolated five-year window during the 1990s. The compounding that created genuinely exceptional wealth happened over 15, 20, and 30-year periods, not five-year ones. The mathematics of compounding are front-loaded only in textbook examples. In practice, most of the wealth in a compounding series accumulates in the later periods, precisely because the base has grown so large.

The second problem is taxes. Each five-year exit triggers a taxable event on the accumulated gain. That tax payment removes capital from the compounding base permanently. The reinvestment starts smaller than it would have if the position had been held. Over multiple cycles, this drag is substantial. Research on this effect suggests that a long-term holder in a taxable account can keep meaningfully more capital working simply by deferring realizations, even if both the flipper and the holder own identical underlying businesses.

The third problem is redeployment risk. To justify selling a great business every five years, you need to find a comparably great business to replace it, at a reasonable price, in a consistent and repeatable way. This is extremely difficult. The tax cost of the exit is a certain loss. The gain from the new position is uncertain. The expected value of this exchange is negative for most investors in most market environments.

The Algebra of Compounding Over Long Horizons

A simple numerical illustration makes the point concrete. An investment growing at 12 percent annually will roughly double every six years. After 12 years it has quadrupled. After 30 years it has grown by a factor of approximately 30. The gain in the final decade of that 30-year hold is larger in absolute dollar terms than the gain in the entire first two decades combined. This is why Buffett has described his favorite holding period as forever. It is not sentiment. It is arithmetic.

Berkshire’s own stock price history reflects this. The per-share book value of Berkshire grew from roughly $19 in 1965 to values measured in hundreds of thousands of dollars over the following six decades, a compounding rate that Buffett has publicly disclosed in Berkshire’s annual letters. The compounding rate itself was not dramatically higher than what a skilled equity manager might achieve. What was dramatically different was the duration over which it was sustained without interruption.

The length of the compounding runway matters as much as the rate. A 15 percent annual return sustained for 40 years produces a fundamentally different outcome than the same rate sustained for 10 years, not just a larger one, but one that operates on a completely different scale.

This is not a subtle point, but investors repeatedly discount it because the benefits are invisible for the first decade or more. The compounding that makes a position genuinely transformative sits in year 20 or year 30, and most investors never get there because they exit in year 5 or year 8 for reasons that feel rational in the moment: the stock has “run up,” the valuation “looks full,” there is a “better opportunity elsewhere,” or simply because patience has run out.

The Behavioral Architecture That Made It Possible

Understanding why Buffett was able to hold when others could not requires looking at the structural and psychological conditions he built around himself. He ran a closed-end vehicle, Berkshire Hathaway, which meant investors could not redeem their capital on demand and force him to sell. He did not manage a mutual fund subject to quarterly outflow pressure. He was not accountable to a benchmark that might diverge painfully from his holdings for a few uncomfortable years. He controlled his own capital and reported results annually in a letter that emphasized long-run thinking explicitly.

These structural advantages are not easily replicated by an individual retail investor, but the behavioral discipline they enabled absolutely can be. The lesson is not that you need to find the next Coca-Cola. It is that if you do own something with genuine long-term merit, whether that is a single quality company or a broad index fund tracking the MSCI World or the S&P 500, the act of holding through volatility is itself the value-generating action. The holding is not passive in the sense of being effortless. During multiple market cycles, holding requires active decisions not to sell. That is the skill Buffett demonstrated most consistently.

Behavioral finance research consistently shows that individual investors underperform the funds they own because they buy after strong performance and sell after poor performance. The fund itself may return 8 percent annually over a decade while the average investor in that same fund earns closer to 5 percent, purely because of timing decisions around entry and exit. Buffett’s record, seen in this light, is partly a story of someone who simply refused to make that mistake at scale.

What This Means for Index Investors

The lesson from Buffett’s holding period record is directly applicable to someone who has no interest in individual stock selection and prefers a broad index fund. The math is the same. The behavioral challenge is the same. The enemy is the same.

An investor who bought a low-cost S&P 500 or MSCI World index fund in any year from the early 1990s to the mid-2000s and held without interruption through the dot-com crash, the global financial crisis, and multiple subsequent corrections would have generated returns that look extraordinary in hindsight. The fund itself required no skill to select. The only required competency was staying in it during the periods when selling felt most justified.

This is where Buffett’s patience lesson translates most cleanly. You do not need to identify the next Coca-Cola. You do not need to read balance sheets or estimate intrinsic value. You need to make a reasonable initial allocation to a diversified, low-cost index vehicle and then behave like Buffett behaved with his best positions: hold through the noise, resist the urge to act on short-term information, and let the compounding run for as long as your timeline allows.

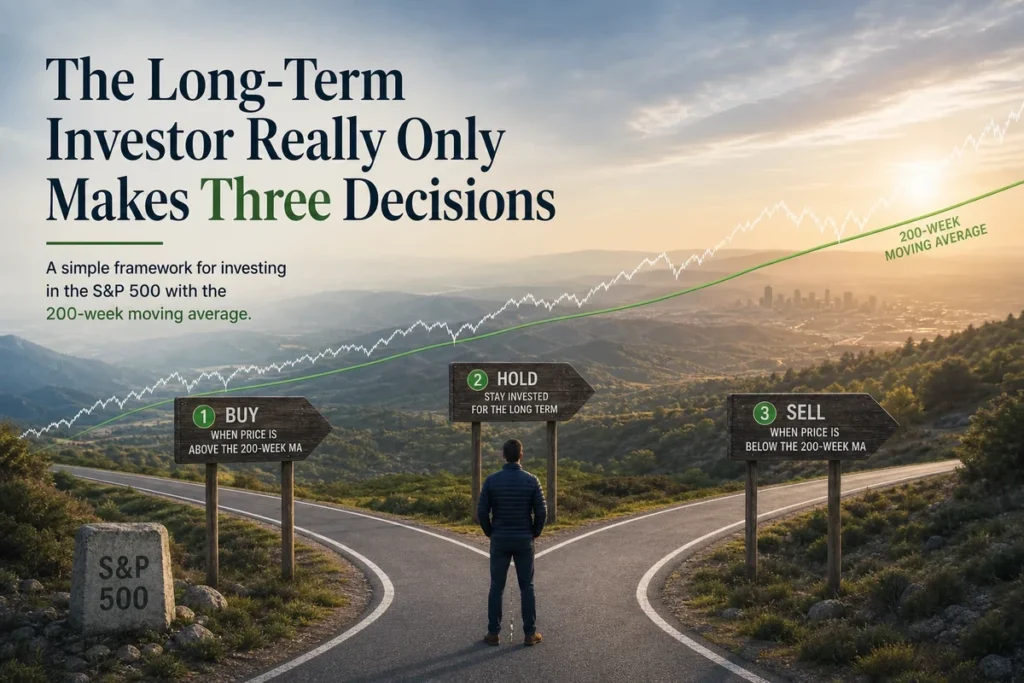

The 200-week moving average framework used at this site is useful as a long-cycle signal for identifying extended periods of genuine trend deterioration. But it is not a tool for trading around normal volatility. Its value is precisely that it operates on the same long time horizon that made Buffett’s approach work: filtering out noise and responding only to meaningful structural shifts in market direction.

The One Edge Anyone Can Copy

Buffett’s other advantages are not reproducible. His access to private deals and preferred stock structures, his use of Berkshire’s insurance float as effectively zero-cost leverage, his brand and reputation that bring unique opportunities to his doorstep, his decades of pattern recognition across business cycles: none of these can be packaged and handed to an ordinary investor.

Patience can be. It is free. It requires no analytical training, no Bloomberg terminal, no proprietary data feed. It does require something harder to sustain: genuine indifference to short-term price fluctuations, a written investment plan that anticipates volatility, and a willingness to look wrong for extended periods before being proven right.

The investors who have most consistently benefited from Buffett’s framework are not the ones who tried to replicate his stock selection. They are the ones who absorbed his attitude toward time. Charlie Munger, Buffett’s longtime partner, made this point with characteristic directness: the big money is not in the buying and selling but in the waiting. Not the waiting for a catalyst or a price target. Simply waiting, while the business or the index beneath you continues doing what growing enterprises do over long periods.

Patience in investing is not the absence of action. It is the repeated, deliberate choice not to interrupt compounding when nothing fundamental has changed. That choice, made consistently over decades, is the actual edge.

For a long-term investor today, the practical implication is straightforward. Review your portfolio not for what to buy next but for what you are at risk of selling prematurely. The positions you are considering exiting because they feel flat, because a recession is anticipated, or because some macro uncertainty has made you uncomfortable: these are often the positions that most need to be held. The exit is rarely the right move. The compounding that will define your long-run result is usually still in front of you, not behind you.

Frequently Asked Questions

Q: Didn’t Buffett also make mistakes by holding too long, such as with certain newspaper investments?

A: Yes, and that is an honest qualification. Patience is valuable when the underlying business retains its competitive position. Buffett has acknowledged that he held some businesses past their structural peak, newspapers being a clear example. The lesson is not to hold blindly forever but to distinguish between temporary price weakness in a fundamentally sound business and genuine permanent impairment of the underlying enterprise. That distinction is the actual analytical work required.

Q: How does this apply to someone holding a broad index fund rather than individual stocks?

A: The application is actually cleaner for index investors. A diversified index fund continuously refreshes its composition as the economy evolves, removing failed businesses and adding emerging ones automatically. The case for holding it through volatility is stronger than for any single stock, because permanent impairment of a broad economy-tracking index requires an outcome far more extreme than the failure of any individual company.

Q: What holding period is long enough to capture the compounding benefit described here?

A: Research on equity market returns suggests that 10-year holding periods have historically eliminated most instances of loss in diversified index portfolios, and that returns over 20-year periods have been consistently positive across most major global markets. Buffett’s framework suggests thinking in decades rather than years, but even extending a typical holding period from 3 years to 10 years captures a meaningfully larger share of the long-run compounding curve.

Q: Is the 200-week SMA relevant to this patience-based approach?

A: The 200-week SMA is a long-cycle tool designed to identify when an extended structural downtrend may be underway, which is a materially different signal from normal year-to-year volatility. Used correctly, it supports the patience framework by filtering out noise that would otherwise trigger premature exits. It is not a substitute for the fundamental commitment to long holding periods but rather a secondary check that can help investors distinguish true trend breaks from uncomfortable but temporary drawdowns.